- Colony Capital Founder & CEO Thomas Barrack to Step Aside Following Activist Blackwells Capital’s Influence

- Strategy Shift from Digital Bridge Acquisition Indicates Colony is Worth at Least $12.74 per Share in Sum of the Parts Analysis

- Blackwells Capital Likely to Nominate an Additional Four Directors to Board

Colony Capital Inc. has taken one step in the right direction with a decision to focus on digital infrastructure and real estate asset management. The question is whether it can stay dedicated to that business strategy, shed non-core assets, and avoid falling prey to vanity projects in Hollywood or elsewhere.

Several days after a recent analysis in July by CorpGov that first reported activist investor Blackwells Capital may seek to replace board directors and refresh management at Colony, the struggling real-estate company said CEO Thomas Barrack would step down as part of a strategic shift. The plan is to become the leading alternative asset manager focused on both real estate and digital infrastructure such as cell phone towers and data centers.

Colony simultaneously announced it would pay $325 million for privately-held global asset manager Digital Bridge, which oversees $20 billion in digital infrastructure assets. The deal would increase Colony’s assets under management to about $60 billion, while allowing it to remain structured as a real estate investment trust (REIT).

According to a person familiar with the matter, Blackwells intends to continue to pressure the company to do what is in the best interest of shareholders. The person said that Blackwells will likely nominate four or more directors during the upcoming window in November, in addition to the three new directors that the New York-based activist put on the board earlier this year. Should Colony not show more substantial progress in its turnaround beyond the recent succession plan announcement, executive management could face considerable pressure, the person said.

Colony and Blackwells both declined to comment to CorpGov.

Several shareholders who spoke to CorpGov on the condition of anonymity expressed concern about the lack of proper oversight at the board level, given that Mr. Barrack and multiple directors were at the helm while the company lost its way in recent years. There is also concern among these investors that Mr. Barrack has become a liability for the company given recent media reports about his alleged nuclear dealings in Saudi Arabia and an inquiry by federal prosecutors into possible foreign influence on President Trump’s campaign. Mr. Barrack played a major role in the Trump campaign and is a friend of the President, but he has not been accused of any wrongdoing.

Shares of Colony have fallen from about $15 to $5 since 2017, when the company merged with two other REITs in a deal that was purported to have underpinnings in strong corporate governance but quickly unraveled. That led New York-based Blackwells, which had been working with company since 2018, to sign a cooperation agreement in early 2019 with Colony that led to the nomination of three new Directors as well as the formation of a Strategic Asset Review Committee tasked with “reviewing, evaluating and making recommendations to the Board on issues related to the Company’s assets and business configuration.”

As for Colony’s latest moves, it should be noted there is significant good news and potential shareholder value creation from the Digital Bridge deal. Colony announced that Mr. Barrack would be replaced as CEO by Marc Ganzi who is Co-Founder and CEO of Digital Bridge. The change of CEO indicates the company is willing, in theory, to let a new leader take it in a better direction.

Also, Colony has set its sights on becoming a leading pure play, alternative asset manager in the public equity markets focusing exclusively on real estate and digital infrastructure. That indicates it may exit its asset-heavy real estate businesses and other non-core divisions.

Colony will become one of the biggest players in real-estate asset management. Pro forma for the acquisition and another pending deal, it should soon have approximately $40 billion of fee-earning assets under management. If the asset manager can begin growing fee-earning assets at $10 billion a year as Mr. Barrack has suggested, Colony will soon be the third-largest publicly-traded real estate alternative asset manager only behind Brookfield Asset Management (ticker: BAM) and Blackstone (ticker: BX) while significantly ahead of Apollo (ticker: APO), Ares (ticker: ARES), Carlyle (ticker: CG), KKR (ticker: KKR), Oaktree (ticker: OAK) and Och-Ziff (ticker: OZM).

The deal also tilts Colony toward a more attractive industry mix. With Digital Bridge, Colony’s asset manager will be more-than 50% focused on digital infrastructure real estate assets, among the most sought-after areas for REIT investors. Publicly-traded cell tower companies (tickers: AMT, SBAC, and CCI) are some of the best-performing REIT stocks of 2019 and trade at some of the highest valuations in the industry: AMT, for instance, trades at 28 times adjusted funds from operations (AFFO), according to Sentieo. In turn, REIT investors in cell phone towers and data centers (tickers: DLR and INXN) may gravitate to Colony.

Colony can also follow Blackstone’s playbook from 2008, when it purchased credit fund manager GSO. Since then, Blackstone’s extensive relationships with limited partners have allowed GSO to flourish from approximately $10 billion assets under management to roughly $140 billion today. Together with Colony, Digital Bridge should also grow assets faster, particularly if they introduce new products as Blackstone and GSO have done.

How much are Colony shares worth after the Digital Bridge deal? Digital Bridge is described as managing $20 billion in assets, but some of those are tied to an upcoming deal to acquire communications infrastructure company Zayo Group Holdings (ticker: ZAYO) and others are shared with Colony. To be conservative, assume the acquisition of Florida-based Digital Bridge will immediately bring in $9 billion in fee-earning assets, the amount the company discloses.

Next, apply reasonable assumptions of a 1.5% management fee, a 50% Ebitda margin, and a 20% tax rate. That results in net income of $54 million. Put on a multiple of 20 times, the Digital Bridge income is worth $1.08 billion, making Colony’s pro forma asset management group worth $2.7 billion.

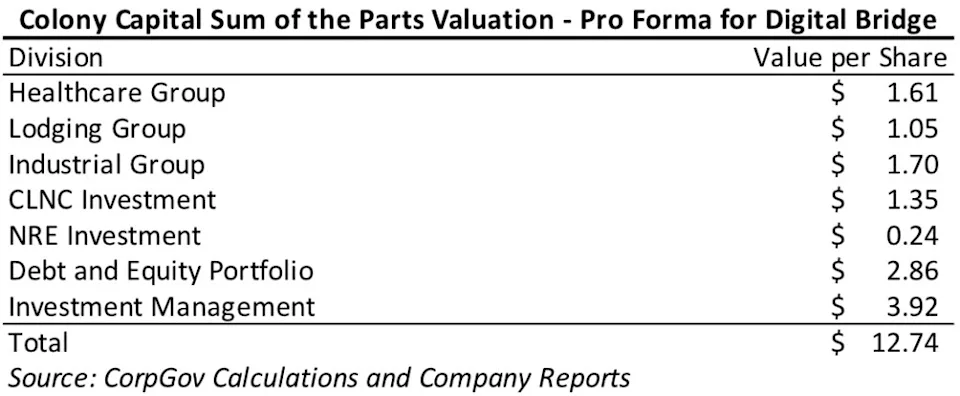

Using the same sum of the parts approach in CorpGov’s earlier analysis, the updated valuation for the entire company, including the cash and new stock issuance in the acquisition, is $12.74 a share versus a previous calculation of $11.15 a share. Of that valuation, nearly $4 is attributed to the asset management division. With the stock trading at about $5.40, the market is arguably ascribing very little value to other six remaining assets of Colony: three REITs, a 37% interest in publicly traded CLNC, an 11% interest in publicly traded NRE and a $2 billion portfolio of real estate debt and equity securities.

The stock also should have limited downside in the near term. Colony pays an attractive 8% dividend yield, all the more appealing now that the Federal Reserve has cut rates.

Despite all that, the market isn’t so impressed, with the stock trading up only about 10% after the announcement and recently giving some of those gains back. While sell-side analysts generally applauded the deal, none raised their price targets. Part of the problem lies in concerns about execution. Sell-side research analyst Jade Rahmani of Keefe, Bruyette & Woods wrote that “significant work is still needed across CLNY’s disparate asset base (in many cases over a period of years), so the evolution of CLNY’s new strategy will take time.”

Indeed, there are serious obstacles to realizing Colony’s full value. For one, the company continues to own many assets that would be better off in other hands. These assets have no apparent synergies with the alternative asset management business and if the company doesn’t take more aggressive action or outline firm plans to dispose of them, the stock may continue to languish.

There is also the issue of poor capital allocation under current management. Colony has repurchased few shares in 2019 despite the stock trading at a deep discount to CorpGov’s NAV estimates and those of most sell side analysts. With the stock trading around $5 for much of 2019 prior to the recent deal announcement, there was ample opportunity to repurchase shares. That decision makes it hard to feel confident in the current board and management.

Equally important are the issues of leadership, oversight, and corporate governance. Following the CEO transition, Mr. Barrack will remain on the Board as Executive Chairman of the company. The vague – and extended – timeframe of 18 to 24 months for his transition should give investors pause. Public company CEO transitions of such long duration are rare.

The reality is that even after Mr. Barrack becomes Executive Chairman, he will likely have an outsized influence over management decisions. Given his track record as the architect of the three-way merger and willingness to take a hefty $25 million salary over the last three years, he doesn’t belong in the driver’s seat any longer.

What’s more, Mr. Barrack could get in the way of what appears to be a powerful incentive for Mr. Ganzi to do a good job. As part of his compensation package and employment agreement, Mr. Ganzi will receive 10 million additional Colony shares if the stock rises above $10 – a potential $100 million payout. While Mr. Ganzi should feel motivated to take decisive action, Mr. Barrack could easily interfere.

The only sure way to give Mr. Ganzi the freedom to perform would be for Mr. Barrack to step aside much sooner. For instance, if he moved to a role of non-executive director, Mr. Barrack might give investors the comfort they need.

In the meantime, Mr. Barrack is apparently still distracted by investments that have nothing to do with real estate or digital infrastructure. In late July, an article with a lead byline from a respected M&A journalist indicated that Colony was exploring a minority investment in Legendary Entertainment, a Hollywood studio owned by China’s Dalian Wanda.

An investment in Legendary is concerning on multiple levels. First, Dalian Wanda has been shedding low-quality assets recently such as media company Wanda Sports (ticker: WSG). The company, which manages sports rights, had an abysmal IPO in late July, flopping 36% on its first trading day even after the offer price was slashed. The shares have continued to slump since then. Dalian Wanda is a motivated seller because of government pressure to reduce leverage, but it’s unlikely to sell its crown jewels.

Hollywood is notorious for luring outside investors into the movie business so they can enjoy the glitz of the red carpet – even if the investments are otherwise unattractive. The industry is extremely risky, and production companies like Legendary depend on the success of a small number of blockbuster films while many projects lose money.

It’s also worth pointing out that Mr. Barrack threw Harvey Weinstein’s company a financial lifeline just days after The New York Times exposed the alleged sexual predator. “We are pleased to invest in The Weinstein Company and to help it move forward. We believe the Company has substantial value and growth potential,” Mr. Barrack said in an October 2017 press release. “We will help return the Company to its rightful iconic position in the independent film and television industry.”

Colony ultimately backed out of a financing deal after a diligence process, avoiding what would have been a catastrophic investment as The Weinstein Company ultimately went bankrupt. Even so, the experience is a good indication of the financial danger of investing in Hollywood.

In fairness, Colony Capital appears to have profited from its 2010 investment in Miramax, which was purchased from Disney in 2010 for about $660 million. But the deal terms were not disclosed when the investment was sold in 2016. A thorough search of SEC filings with Sentieo confirms Colony never disclosed specific financial details about any gains from Miramax. Recent media reports that Miramax is back up for sale indicate a valuation of $650 million, roughly the same value it commanded a decade ago.

Even if Mr. Barrack were a savvy Hollywood investor, the question remains: Why invest in such a distracting asset that has nothing to do with real estate or digital infrastructure? And if there is a chance of more such deals happening, can investors be comfortable owning Colony?

And while Mr. Ganzi appears qualified, the company hasn’t done much to educate investors about him. At the time of announcement, Colony did not hold a public investor call to introduce to Mr. Ganzi to shareholders and analysts or walk them through the Digital Bridge acquisition, which is common practice when there is a significant change at a public company. Mr. Ganzi has no experience running a public company and investors know almost nothing about his approach to managing one.

The company has an opportunity to introduce the incoming CEO on its upcoming earnings call this week on Friday, August 9th. That will also be a chance to delineate more specific plans about shedding assets and shifting power away from Mr. Barrack. Short of that, Blackwells may gain a much stronger hand.

Contact:

John Jannarone, Editor-in-Chief

www.CorpGov.com

Twitter: @CorpGovernor