- Nam Tai Property Inc.’s April 26 special meeting to consider new directors has been postponed by a Caribbean court

- Dissident IsZo Capital Management LP recently raised its stake to 14%

- Nam Tai says funding remains in flux following demand letters, account freezing by Chinese banks

- IsZo says it prefers to keep bank loans, but has “strong relationships with alternative financing sources”

- Finance attorneys familiar with Chinese regulations and not involved with the situation told CorpGov that loans could be challenging to replace

- Billionaire board director and 19% Nam Tai shareholder Peter Kellogg supported special meeting

- ISS recommends to vote for three of IsZo’s six nominees

It’s not your everyday proxy fight. With a cast of characters including 78-year-old billionaire Peter Kellogg, a British Virgin Islands judge, and a throng of Chinese banks holding the purse strings, it sounds more like the script for an international thriller.

Meet Nam Tai Property Inc. (NYSE: NTP), a real estate outfit with a headquarters in Shenzhen, China, a corporate registration in the British Virgin Islands, and shares that trade in New York. The company, whose market capitalization is about $430 million, has come under pressure from New York-based investment firm IsZo Capital Management LP, which is frustrated with the company’s leadership and has nominated six directors to the board. The showdown was expected to reach a climax at a special meeting on April 26, but that has just been delayed by a Caribbean court, setting the stage for more possible drama.

The action first heated up last year, when IsZo, now the largest independent shareholder with 14{% of shares outstanding, initially requested a special meeting. Chief among IsZo’s gripes was that developer Kaisa Group Holdings Ltd. (HKG: 1638), which currently owns 24% of the company and replaced the CEO in 2017, was hurting other shareholders. In an interview with CorpGov, IsZo cited a poor stock performance – negative 57% – in the two-and-a-half years between the day Kaisa’s appointee became CEO and the activist went public with its campaign last May.

Soon after, trouble allegedly began to brew in China with Nam Tai’s mainland banks. According to the company, all of its lending banks were alarmed by the proposed removal of every director but two. One of those directors is Peter Kellogg, a 78-year-old billionaire who sold the eponymous securities clearing and execution firm Spear, Leeds & Kellogg to Goldman Sachs in 2000. The second is Mark Waslen, a former employee who has been a director since 2003.

Nam Tai said its lending banks notified it that “substantial uncertainties would be cast upon the Company’s operations and management control in light of recent actions taken by IsZo and reserved their rights to withdraw their banking facilities.” In one case, Nam Tai in fact repaid $30 million at the demand of a bank, the company said.

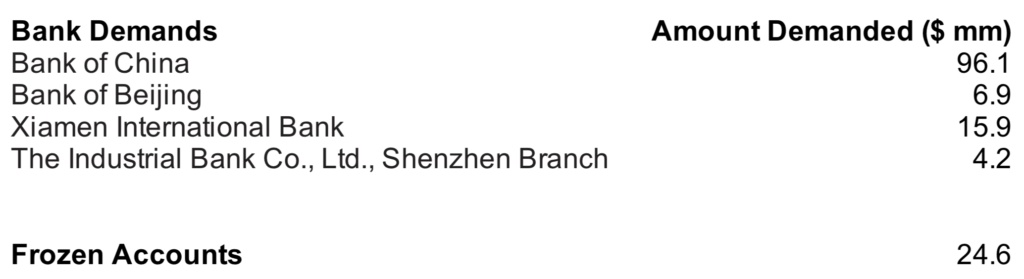

The banks include state-owned Bank of China, Bank of Beijing, Xiamen International Bank, and The Industrial Bank Co., Ltd., Shenzhen Branch (the latter three of which are privately-held). CorpGov emailed executives at all four banks seeking comment but did not receive a reply.

In October, Nam Tai made a controversial move: Facing what it called concerns about access to a “potential liquidity crunch due to withdrawals of the bank facilities” the company raised $170 million from Kaisa and another investor through a so-called PIPE offering of new shares. While the maneuver appeared to protect the company from liquidity constraints, IsZo points out that it gives enormous voting power to Kaisa, which bought most of the newly-issued shares.

His Lordship, the Hon. Justice Adrian Jack (left in red with wig)

For a while, it appeared that IsZo had a clear upper hand – especially after a key court ruling. In early March, His Lordship, the Hon. Justice Adrian Jack of the Eastern Caribbean Court held that the private placement was void and teed up the special meeting. Justice Jack excoriated Nam Tai’s management team for attempting to entrench themselves and even went as far as to scold Nam Tai’s attorneys.

Nam Tai claims that the ruling triggered even deeper concerns among the Chinese banks. Rather than reserving their rights, the banks actually demanded repayment to the tune of $123 million, Nam Tai said in a disclosure. Additionally, about $24.6 million in deposits have been frozen, the company said.

Those requests, made in early March in the days after Justice Jack’s decision, were for five-day payments. It is notable that the banks have not enforced remedies as of yet in Chinese court. The reason is unclear but it’s possible they were awaiting the outcome of the special meeting.

Source: Nam Tai

In a surprising twist, the Eastern Caribbean Court of Appeal last week announced that the special meeting would be postponed. The court didn’t overturn Justice Jack’s decision but will review it under an appeal.

It is conceivable that the Court sides with Nam Tai, in which case the activist would probably struggle to win given that Kaisa would have nearly half of the voting shares. But if the Court sticks with Justice Jack’s decision, the dissident has sufficient votes to win all six seats.

However, the drama may not end there. If indeed the banks seek to enforce their demands, Nam Tai could find itself in a tough spot.

For its part, IsZo says it would like to work something out with the existing banks. “We know how valuable Nam Tai’s relationships are with its lending banks,” IsZo said in a recent press release. “This is why we intend to have the Company honor all of the terms and obligations, including repayment at maturity, under its existing loan agreements in good faith. Although we have strong relationships with alternative financing sources, we prefer that the Company retains its existing banking relationships.”

But if Nam Tai’s statements in SEC filings about the demand letters are taken at face value, it appears IsZo would have its work cut out winning the banks over.

Where else could Nam Tai go for the cash? CorpGov interviewed multiple securities attorneys who are not involved in the situation but are well-versed in Chinese banking rules and practices. Those attorneys said a company that loses its bank financing in China could face challenges restoring it. In particular, other domestic banks, whether state-owned or private, may be reluctant to step in where other well-known banks are unwilling to lend.

That leaves the possibility of finding a foreign lender. For instance, Western banks have branches in China. But as one of the attorneys pointed out, balance sheets of onshore branches of foreign banks tend to be very limited by the Chinese government. Any move to overextend could jeopardize important banking licenses.

An offshore loan attached to a property would also be unusual, these attorneys said. China’s National Development and Reform Commission tracks how much offshore entities lend.

Even if it’s possible to structure a debt deal with an offshore borrower, there’s the question of whether anyone would even want to take the risk. A big concern would be trying to enforce any claims on assets like apartment buildings which serve an important social role – housing people.

Indeed, there has been some activity involving foreign investors purchasing non-performing loans from Chinese banks, but those too can be problematic. The Wall Street Journal recently put it thus: “Investors should consider where they sit in China’s political economy: at the bottom. When authorities have to weigh different interests like those of local banks and companies, or employment against those of a largely unknown foreign investor, buyers shouldn’t be surprised when they come dead last.”

Another solution: Raise equity rather than debt. It also appears Mr. Kellogg, who supported the special meeting proposed by IsZo, could help explore financing. His own net worth is estimated at $3.6 billion by Forbes, meaning he could even shore up Nam Tai’s financing out of his own pocket – were he so inclined. And the amount of leverage on the company’s assets is by no means excessive, so there could be appetite. Mr. Kellogg could not be reached for comment.

But equity comes with its own costs. Either the PIPE or another equity raise to the tune of, say, $150 million would be highly dilutive to a company this size.

A final possibility would be for IsZo and current Nam Tai management to compromise. The company has already taken some modest steps to shore up its governance, with Kaisa-affiliated Ying Chi Kwok stepping down as CEO and Chairman. Dr. Lai Ling Tam (who is affiliated himself with Kaisa) has been appointed Executive Chairman of the Board and should begin more investor-friendly practices, such as improved disclosure and shareholder engagement. But Nam Tai would surely benefit from an extra nudge from some fresh, capable directors.

Proxy advisor ISS suggested shareholders vote for three of IsZo’s six nominees. While ISS agreed with much of IsZo’s arguments, it did point out that IsZo had not made a “thorough critique of the company’s operating performance.”

If the two sides could strike a deal that includes some but not all of IsZo’s nominees (who could give the company a serious boost in corporate governance), it is possible the Chinese bank relationships would remain intact. In that case, there would also be no need for the PIPE or any other capital raise. According to Nam Tai’s latest annual filing, a Board director reached out to IsZo to “express a willingness of the Board to work constructively with IsZo.” As of the date of that filing, April 14, no settlement had been reached.

Contact:

editor@corpgov.com

www.CorpGov.com

Editor@CorpGov.com

Twitter: @CorpGovernor